Are you one of the millions of Americans in default on your student loans? If so, legal developments in 2017 should have you on high alert and ready to seek help from a student loan lawyer.

Student Loan Lawyers Fighting for Consumers

Two 2017 lawsuits have exposed the dark side of the student loan industry already described as unfair and distressful for borrowers and generally out of control. Both cases involve dubious and illegal practices by student loan debt collectors that worked for huge lenders. Continued investigations likely will expose additional illegal practices.

In addition, the federal government reportedly has expanded its privatized collection program. Finally, the Trump Administration plans to consolidate federal student loan servicing under one company. What do these changes mean to you? If you are in default, they make it more likely that you will be sued by the debt collector.

Robyn Smith, an attorney at the National Consumer Law Center, recommended that if you’ve been served with a lawsuit, get an attorney who specializes in debt collection and credit reporting issues. Take the papers to a student loan attorney as soon as possible and before your scheduled court appearance. By ignoring the papers, you literally give the creditor a default judgment against you.

Investigation in the National Collegiate Case Showed That Some Debtors with a Student Loan Attorney Got Their Cases Dismissed for Lack of Evidence

The Consumer Financial Protection Board (CFPB) charged National Collegiate, which services private student loans, and its debt collector Transworld for filing lawsuits against borrowers based on false or misleading documents. According to the Washington Post, the CFPB investigation showed that Transworld filed 95,000 lawsuits nationally, including 2,000 without proof of ownership of the debt, resulting in a recovery of $21 million in judgments. Student debt lawyers won dismissals for their clients in New Hampshire, Ohio, and Texas based on Transworld’s lack of necessary documentation.

As part of a consent order, the two companies agreed to pay damaged borrowers $3.5 million. If you are a National Collegiate customer, contact the CFPB or a student loan attorney to determine if you are eligible for damages.

If You Are a Navient Customer You May Want to Consult a Student Loan Attorney to Learn If You Have a Claim Against the Company

The CFPB and three states have sued Navient, the largest servicer for student loans, for alleged illegal activity which cost borrowers millions

According to a New York Times article, Illinois Attorney General Lisa Madigan said that the misdeeds could affect every customer and that damages could be billions of dollars. Navient collects payments on private and government loans for banks, the government, and other lenders.

Reportedly, the allegations include cheating borrowers out of their rights to lower payments, defaulting rather than discharging the debts of the totally disabled, and steering borrowers away from cheaper income-based repayment plans.

Consult a School Loan Attorney If You Believe a Student Loan Debt Collector Is Acting Illegally

Student loans burden 88 million Americans. Borrowers should not be exploited by greedy or incompetent loan servicers or their debt collectors.

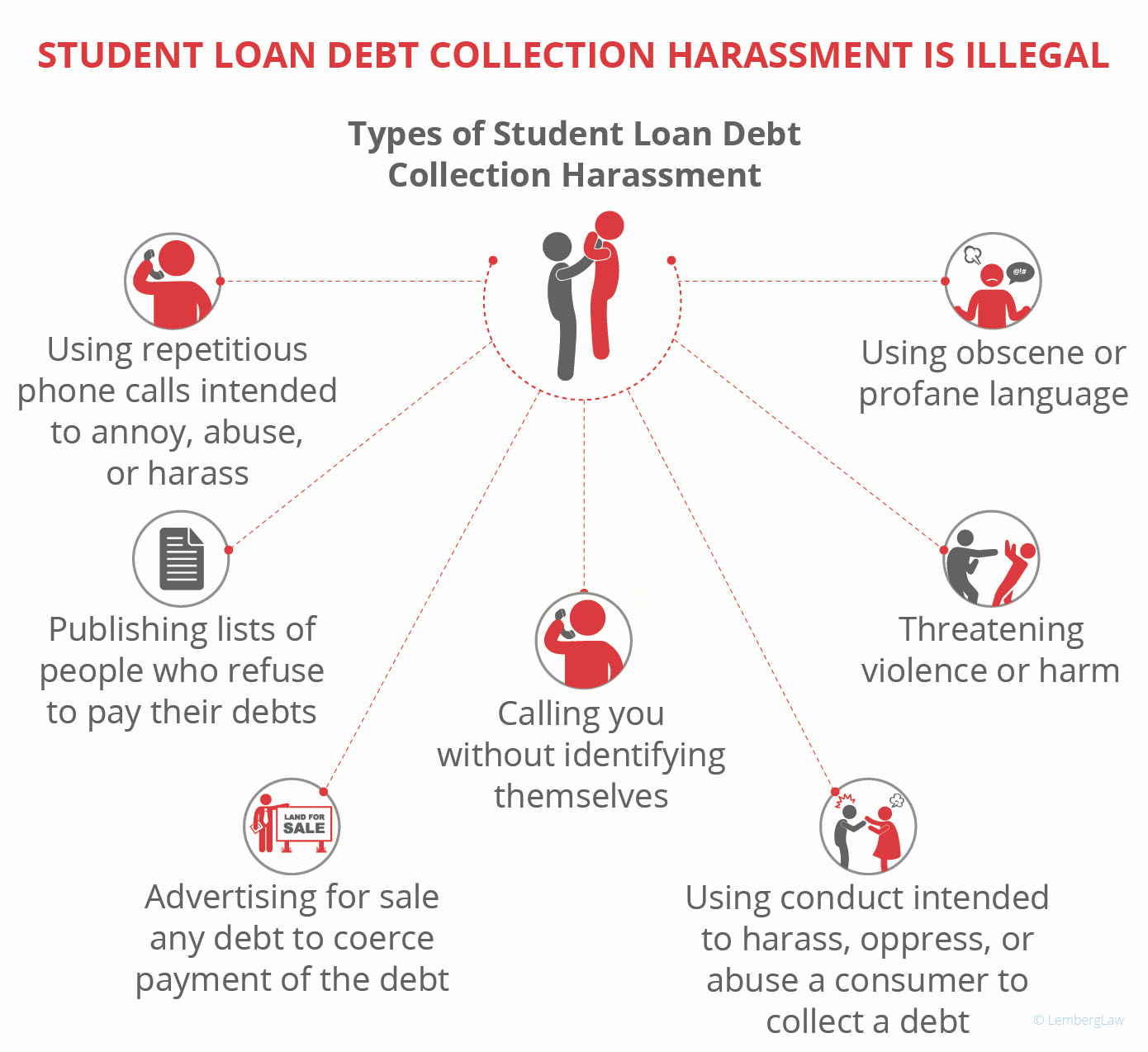

The Federal Debt Collection Protection Act (FDCPA) applies to collectors of school loan debts. The FDCPA specifically forbids these collection activities:

The use of conduct which is likely to harass, oppress, or abuse a consumer regarding the collection of a debt.

The use or threat of use of violence or other criminal means to harm the physical person, reputation, or property of any person.

The use of obscene or profane language or language the natural consequence of which is to abuse the hearer or reader.

The publication of a list of consumers who allegedly refuse to pay debts, except to a consumer reporting agency.

The advertisement for sale of any debt to coerce payment of the debt.

The act of allowing a telephone to ring or engaging any person in telephone conversation repeatedly or continuously with intent to annoy, abuse, or harass any person at the called number.

The placement of telephone calls without meaningful disclosure of the caller’s identity

Congress passed this law to protect you from any type of debt collector harassment. If you are uncertain whether or not a debt collector harassing you, contact an attorney who is experienced in protecting your rights under the FDCPA.

If a debt collector has been hounding you, to speak with a representative directly and immediately call 844-685-9200 for a free, no-obligation case evaluation. Our attorneys have experience in assisting those with student loans, fighting debt collectors, and standing up for consumers. If a debt buyer has violated the Fair Debt Collection Practices Act, you’re entitled to file suit in federal court and could be awarded up to $1,000 and other damages.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."

i’m a victim of student aid loan fraud by the stenotype institute school of court reporting the owner went to prision for fraud stealing student loan money from the students who had to quit school within a month of enrolling .students never recieved their money back and are in debt to nelnet in linolon nebraska who damaged our credit reports for student us dept of education loans we never used or recieved or education we never gotten. our loans should be discharged, and removed off our credit reports but the us dept of education and nelnet refuse to help i contacted the FBI FOR HELP

Shanna

I graduated from Branford Hall Career Institute on New Karner Road in Albany, NY in 2011 for medical coding and billing. When I graduated I was promised an internship, free classes if I needed to come back for any training in the future after I graduate, and a job after I graduate. I had to find my own internship, I never was able to find a job, they never helped me either, and they closed down for good because they could not pass the accreditation so I can not go back to school for the training that I need for ICD-10 coding since I graduated with the training of ICD-9. They never sent me anything in the mail or contacted me and they started to garnish my wages. I was wondering if I qualified for a discharge. Thank you

Susan s

I had a student loan 10 years ago, had to leave school because of the onset of a medical condition, at that time all money owed the school was paid, the amount of the difference that the state sent to the school minus one day was sent back to the state. I do have my receipt that Sallie may was paid in full. Navient lied to me for years, they put it on my credit report which lowered that drastically, it then came off my credit report, today I get a call from icr stating I owe the government 9000 dollars and how would I like to pay it. They said I am refusing to pay the federal government, which I paid them once how many times do I have to pay then???? Please help this has been going on for over 10 years

C. O

Have/Had Navient as my Student Loan Servicer, and the level of unprofessionalism is absurd! I had to stop attending school due to disabling health problems, and have been using Deferments and Forbearance to avoid having to make payments. I have not been able to work so have no income what so ever!

Numerous times, I had to contact Navient because even though they are the servicer on ALL my loans, I would receive late payment notices even though I received other noticed stating that I had a deferment or Forbearance!

Now, it gets even worse because our tax return was garnished this year because I am now said to be in DEFAULT! Again, I have NO income so they actually took what is “my husband’s tax refund” for MY debt!

Toward the end of last year, I filled out the Income Driven Payment Forms and thought I was good for about a year, but NO-I’m I’m DEFAULT because NAVIENT OBVIOUSLY DIDN’T DO THEIR PART IN THE PROCESS!

This is SO completely unfair! I also recently found out that Navient SHOULD HAVE told me about the Income Driven Plans previously, but I had to find out about it ON MY OWN, THEN, they don’t even process it! I seriously hope the government allows student loan holder to sue Navient!

They are ruining people’s lives! I have to now go tack down my loan and do some type of consolidation (and pay all the FEES associated with that) to get my loans back on track, and then TRY AGAIN to get on a program I ALREADY TRIED TO GET!

I also now have this on my credit report because is Navient’s negligence! Is there EVER an recourse for the damage they inflict upon others!?

Matthew H

1)1990, 1992, 1993 I was promised college funds by wealthy Grandparents. Then was never not paid, So, Govt. pursued the money after it was transferred to family trust. They were fined HUGE. Then had nerve to as for 2nd set of docs to ‘prove’ they were paying on debt, But in fact did not. After paying for cousins Rm/Brd/Cars and college they started sending month amt.. which they sent to all cousins as well in 2009. Navient (Second loan other person.. on my credit) took forms falsely after declining a loan and used old forms to give new loan (after declined early on). I have their lies are on recording… 2) Navient would not renew IBR when they used to do it verbally and now have hiked our debts to $72,000 after working for 20+ years to get it down to $50,000 in less than two years and did the same to my wife. This being after IRS tax mistakes by an tax filing company. Payments so high I could not pay and wife’s doubled. But, I always sent them something till now.

Christy S

I have a student loan that is in garnishment with PCR despite all of my documents stating that my loan was deferred with first payment not due until March 2017. I appealed (desputing: accuracy, unfair reporting practices, and because I had proof that ACS applied and granted deferment & they had no basis to collect. All I asked for was for them to correct the information, make it right and send my loan back to ACS). They denied my claim stating “it was in default before applied deferment anyway…” Garnishment began in July 2017. [Proof with documentation, that ACS granted & applied deferment.] what I didn’t know: [ACS failed to apply in school deference when I was in school; ignoring proof of in school active status from self report (sealed transcripts sent/received) and direct letters & contact from my school’s registrars office.] PCR used this information as basis that I was not credible and “in default anyway…” Since then, harassment at work, home and constant feelings of shame and humiliation riddle me with despair and defeat. The civil suit in WA seems to be in a state of paralysis & complaint filed with BBB has issued no resolve.

Charles W

I found out that I was hit with a default student loan account which I did not apply for. The loan turned out to be in my son’s name. I have never had a student loan, ever. I obtained a law firm to send the collection agency a letter requesting any and all documents bearing my signature requesting the loan and they could not provide any. Their statement was it was all electronic. I made it clear to them I did not authorize any loan or anything else. but they are not cooperating. This was a year and a half ago.

Jeremy B

I had a couple of federal loans through Navient that was apparently transferred to USAfunds without my knowledge in December 2017. I have been paying on the private loans on a rate reduction program while keeping all the other loans on forbearance. Unfortunately, they are trying to garnish my wages on two of the federal loans because it is default. My question is how is it in default? From December 2017 to today June 6 2018, is not 270 days and I was never notified. The only reason I am aware is because I received a letter from my payroll department about the garnishment. What kind of shady and illegal activity is Navient and United Student Aid Funds up to? Why would I let it go to Default when I have been using the Forbearance method? Now, Navient or USA funds are not willing to work with me to get my account back into good standing. These PEOPLE need to be stopped from ruining peoples lives.

Are you one of the millions of Americans in default on your student loans? If so, legal developments in 2017 should have you on high alert and ready to seek help from a student loan lawyer.

Are you one of the millions of Americans in default on your student loans? If so, legal developments in 2017 should have you on high alert and ready to seek help from a student loan lawyer.

i’m a victim of student aid loan fraud by the stenotype institute school of court reporting the owner went to prision for fraud stealing student loan money from the students who had to quit school within a month of enrolling .students never recieved their money back and are in debt to nelnet in linolon nebraska who damaged our credit reports for student us dept of education loans we never used or recieved or education we never gotten. our loans should be discharged, and removed off our credit reports but the us dept of education and nelnet refuse to help i contacted the FBI FOR HELP

I graduated from Branford Hall Career Institute on New Karner Road in Albany, NY in 2011 for medical coding and billing. When I graduated I was promised an internship, free classes if I needed to come back for any training in the future after I graduate, and a job after I graduate. I had to find my own internship, I never was able to find a job, they never helped me either, and they closed down for good because they could not pass the accreditation so I can not go back to school for the training that I need for ICD-10 coding since I graduated with the training of ICD-9. They never sent me anything in the mail or contacted me and they started to garnish my wages. I was wondering if I qualified for a discharge.

Thank you

I had a student loan 10 years ago, had to leave school because of the onset of a medical condition, at that time all money owed the school was paid, the amount of the difference that the state sent to the school minus one day was sent back to the state. I do have my receipt that Sallie may was paid in full. Navient lied to me for years, they put it on my credit report which lowered that drastically, it then came off my credit report, today I get a call from icr stating I owe the government 9000 dollars and how would I like to pay it. They said I am refusing to pay the federal government, which I paid them once how many times do I have to pay then???? Please help this has been going on for over 10 years

Have/Had Navient as my Student Loan Servicer, and the level of unprofessionalism is absurd! I had to stop attending school due to disabling health problems, and have been using Deferments and Forbearance to avoid having to make payments. I have not been able to work so have no income what so ever!

Numerous times, I had to contact Navient because even though they are the servicer on ALL my loans, I would receive late payment notices even though I received other noticed stating that I had a deferment or Forbearance!

Now, it gets even worse because our tax return was garnished this year because I am now said to be in DEFAULT! Again, I have NO income so they actually took what is “my husband’s tax refund” for MY debt!

Toward the end of last year, I filled out the Income Driven Payment Forms and thought I was good for about a year, but NO-I’m I’m DEFAULT because NAVIENT OBVIOUSLY DIDN’T DO THEIR PART IN THE PROCESS!

This is SO completely unfair! I also recently found out that Navient SHOULD HAVE told me about the Income Driven Plans previously, but I had to find out about it ON MY OWN, THEN, they don’t even process it! I seriously hope the government allows student loan holder to sue Navient!

They are ruining people’s lives! I have to now go tack down my loan and do some type of consolidation (and pay all the FEES associated with that) to get my loans back on track, and then TRY AGAIN to get on a program I ALREADY TRIED TO GET!

I also now have this on my credit report because is Navient’s negligence! Is there EVER an recourse for the damage they inflict upon others!?

1)1990, 1992, 1993 I was promised college funds by wealthy Grandparents.

Then was never not paid, So, Govt. pursued the money after it was transferred to family trust. They were fined HUGE. Then had nerve to as for 2nd set of docs to ‘prove’ they were paying on debt, But in fact did not.

After paying for cousins Rm/Brd/Cars and college they started sending month amt.. which they sent to all cousins as well in 2009.

Navient (Second loan other person.. on my credit) took forms falsely after declining a loan and used old forms to give new loan (after declined early on). I have their lies are on recording…

2) Navient would not renew IBR when they used to do it verbally and now have hiked our debts to $72,000 after working for 20+ years to get it down to $50,000 in less than two years and did the same to my wife. This being after IRS tax mistakes by an tax filing company. Payments so high I could not pay and wife’s doubled. But, I always sent them something till now.

I have a student loan that is in garnishment with PCR despite all of my documents stating that my loan was deferred with first payment not due until March 2017. I appealed (desputing: accuracy, unfair reporting practices, and because I had proof that ACS applied and granted deferment & they had no basis to collect. All I asked for was for them to correct the information, make it right and send my loan back to ACS). They denied my claim stating “it was in default before applied deferment anyway…” Garnishment began in July 2017.

[Proof with documentation, that ACS granted & applied deferment.] what I didn’t know:

[ACS failed to apply in school deference when I was in school; ignoring proof of in school active status from self report (sealed transcripts sent/received) and direct letters & contact from my school’s registrars office.] PCR used this information as basis that I was not credible and “in default anyway…” Since then, harassment at work, home and constant feelings of shame and humiliation riddle me with despair and defeat. The civil suit in WA seems to be in a state of paralysis & complaint filed with BBB has issued no resolve.

I found out that I was hit with a default student loan account which I did not apply for. The loan turned out to be in my son’s name. I have never had a student loan, ever. I obtained a law firm to send the collection agency a letter requesting any and all documents bearing my signature requesting the loan and they could not provide any. Their statement was it was all electronic. I made it clear to them I did not authorize any loan or anything else. but they are not cooperating. This was a year and a half ago.

I had a couple of federal loans through Navient that was apparently transferred to USAfunds without my knowledge in December 2017.

I have been paying on the private loans on a rate reduction program while keeping all the other loans on forbearance. Unfortunately, they are trying to garnish my wages on two of the federal loans because it is default.

My question is how is it in default? From December 2017 to today June 6 2018, is not 270 days and I was never notified. The only reason I am aware is because I received a letter from my payroll department about the garnishment.

What kind of shady and illegal activity is Navient and United Student Aid Funds up to? Why would I let it go to Default when I have been using the Forbearance method?

Now, Navient or USA funds are not willing to work with me to get my account back into good standing. These PEOPLE need to be stopped from ruining peoples lives.